Debentures serve as a versatile tool for companies in India to raise capital without relinquishing ownership or control.

Understanding the intricate process of issuing debentures is crucial for Indian companies aiming to tap into this form of financing effectively.

From initial planning and credit rating analysis to pricing, marketing, and eventual repayment, each step requires careful consideration and strategic decision-making. Let’s delve into the comprehensive process of how companies in India raise funds through debentures.

How do companies raise money through Debentures?

Debentures are a way for businesses to raise money for a variety of needs, including infrastructure development, acquisitions, working capital needs, and expansion. Debentures provide a different kind of finance without sacrificing control or dilution of ownership.

Let’s now examine the issuance of Debentures.

Initial Planning:

The first step in the bond-issuing process is figuring out how much money is needed, which depends on the issuer’s financial needs and debt management skills. The issuer must verify that they have the resources to pay the principal amount at maturity as well as the interest on a regular basis.

Rating Analysis and Documentation:

It is advised that the company receive a credit rating from a rating agency in order to assist in the issuance of a bond in the market.

After evaluating the issuer’s creditworthiness, credit rating agencies like CRISIL, CARE, and IND assign a rating to the bonds. A higher rating denotes a lower credit risk and suggests that the issuer has a strong ability to pay its debts. The pricing of bonds is directly influenced by these credit ratings. Since investors consider higher credit-grade bonds to be less risky, they usually have lower interest rates. Bonds with weaker credit ratings, on the other hand, need to provide higher interest rates to investors who are prepared to take on the additional risk.

If the company does not currently have a rating, the bank assesses its creditworthiness and provides recommendations for appropriate rating agencies based on the industry. From the first meetings the firm attends with the agencies until the actual preparation of the presentation for the agencies, the bank is in charge of directing and supporting the company throughout this process. Legal paperwork is also created in tandem to guarantee it is ready for use during the surgery. Contracts that specify terms for participating banks as well as the issuer fall under this category. Even though this procedure is methodical and slow-moving, outside lawyers offer invaluable assistance.

Selecting the interest rate, maturity, and type of bond:

The issuer has to decide on the bond’s characteristics, such as whether it will be a fixed-rate bond with a consistent interest rate over the term or a floating-rate bond with an interest rate subject to market fluctuations. Additionally, the issuer needs to determine the bond’s duration (the time until maturity) and set an interest rate that aligns competitively with prevailing market rates for bonds of comparable risk levels.

Engaging Underwriters and Approval from SEBI:

The issuer hires underwriters, usually investment banks, to help with different parts of the bond-issuing process after the preliminary preparation is finished. These underwriters provide support in arranging the bond offering, setting bond pricing, guaranteeing adherence to regulations, and marketing the bonds to possible buyers.

Underwriters aid in the collaborative preparation of the bond prospectus, a vital legal document that outlines bond terms, the issuer’s financial status, and associated risks. In order for investors to make wise selections, this paper is essential.

The issuer needs to get the go-ahead from the appropriate regulatory agencies before the bonds are made available for purchase. For example, corporate bond issuances in the United States require registration with the Securities and Exchange Board of India (SEBI).

Pricing and Marketing:

After clearance, underwriters play a crucial role in identifying purchasers by using their vast networks to promote the bonds to potential investors. Presentations and one-on-one conversations with possible investors may be a part of this campaign.

Bond pricing involves computing the present value of the bond’s future cash flows, which include principal repayment and coupon payments, discounted at a suitable interest rate, which is sometimes referred to as the discount rate. Usually, this rate is established by taking into account both the bond’s perceived level of risk and the interest rates that are currently available on the market.

Conditions in the market have an impact on bond price as well. When interest rates are low, freshly issued bonds with higher coupon rates become more attractive, which raises demand and, ultimately, prices. On the other hand, current bonds with lower coupon rates become less appealing in a high-interest rate environment, which lowers their market price.

Allocation and listing of the Bonds:

Banks provide a distribution list to the issuer, which needs to be approved. Investors are then informed of the sums they have been allotted. Relevant indexes are taken into account while determining the pricing. The bond is then formally listed on the secondary market the next day when the sales team notifies the market of the coupon. From then on, its development is continuously observed.

Receiving Funds and Repayment:

Interest starts to accrue on the bonds after they are sold and the issuer receives the proceeds. The issuer is thereafter in charge of paying the bondholders’ periodic coupon payments and repaying the principal amount at maturity.

Investing in NCDs or bonds can be done in a few ways:

1. Primary Market:During the company’s initial offering, you can directly subscribe for NCDs or bonds. Online resources, certain bank branches, or registered brokers can all be used for this. Before making an investment, make sure to thoroughly read the prospectus.

2. Secondary Market: In the secondary market, investors can also buy and sell NCDs or bonds. Stock exchanges like the NSE and BSE are a good place to achieve this. Use your brokerage account to place purchase orders.

3. Mutual Funds and ETFs: Invest in bonds or NCDs by using mutual funds or exchange-traded funds (ETFs) that focus on fixed-income instruments. These funds provide a diverse portfolio of NCDs or bonds by pooling investor funds. Either directly from the fund house or via a broker, you can purchase units.

4. Online sites:You can invest in NCDs or company-issued bonds through a number of online sites. These platforms offer an intuitive user interface for examining available options, contrasting interest rates, and conducting online investing transactions.

Before investing, one needs to do extensive research, evaluate your risk tolerance, and take into account variables like interest rates and credit ratings. A financial advisor can also yield insightful advice specific to your investing objectives, but with Finzace you can eliminate all that!

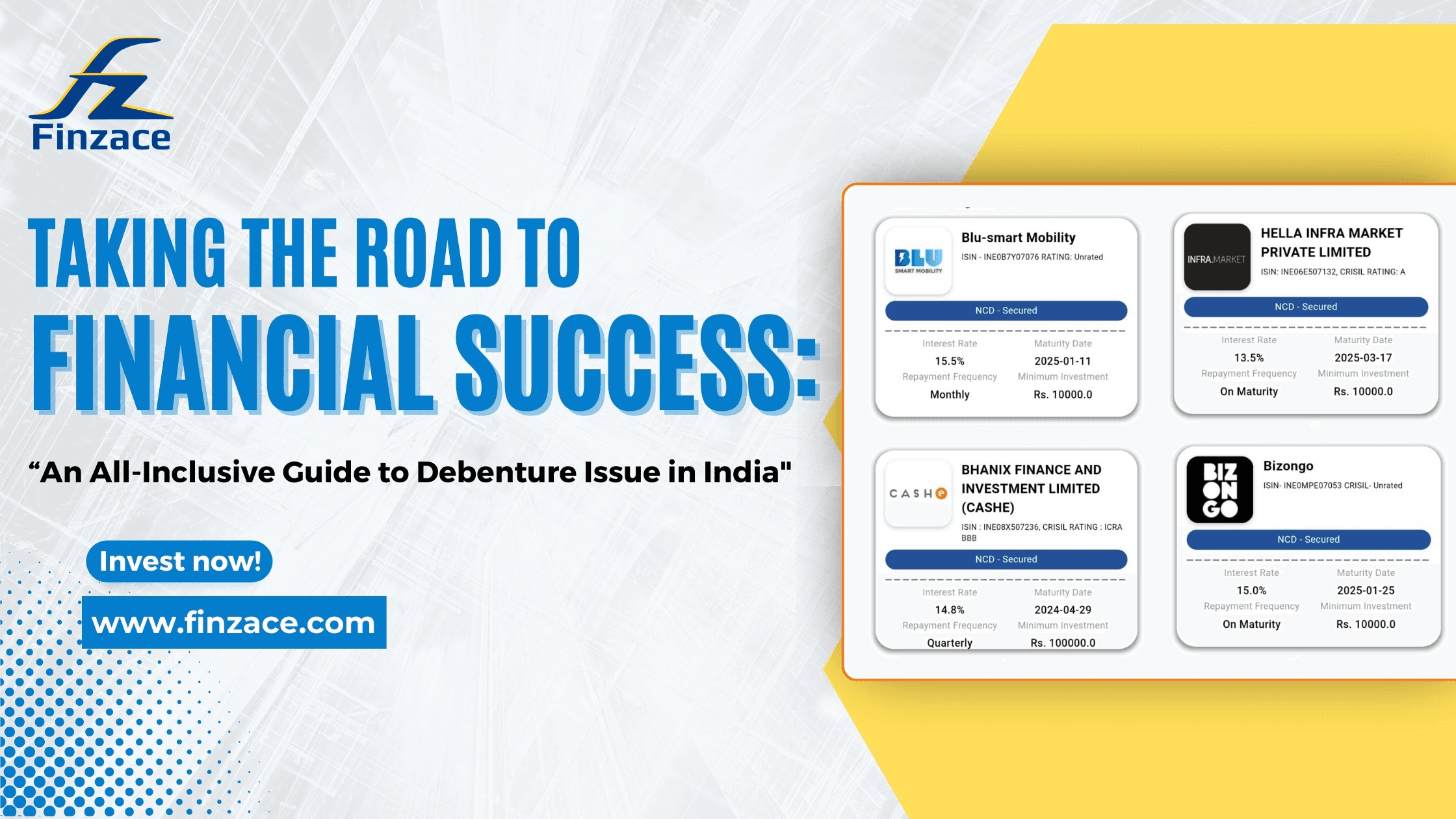

Finzace, however, is the greatest platform for investing in bonds and NCDS!

Finzace offers a simple and easy way to invest in bonds and NCDs. You can choose the secured investment options based on your financial goals and time horizon.

There’s no need to bother or worry—just download the app to see what the best investment possibilities are for you. We provide you with investing choices that are backed by research and assets, taking care of all the work for you.

Download link (Android): https://play.google.com/store/apps/details?id=icreditspace.com

Download link (Apple): https://apps.apple.com/in/app/finzace-earn-12-returns/id6446245952